Buenos Aires vs Montevideo vs Santiago: South America's Cheapest Capital Cities for American Buyers in 2026

Three capitals, three very different deals. Buenos Aires is the cheapest per square meter in all of South America right now, Santiago is the most expensive but the most institutional, and Montevideo sits in the middle with the cleanest legal framework an American can find on the continent. I've spent the last month pulling real listings off ZonaProp, Mercado Libre Inmuebles, and Portal Inmobiliario, cross-checking against the TheLatinvestor Buenos Aires market analysis, the Global Property Guide Chile, and the Uruguayan central bank property price index.

This post is the honest version of the comparison. What $200K actually buys in each. What the closing-cost stack looks like. Whether you need residency to hold title (short answer: no in all three, but with caveats). And which city makes sense for which kind of American — the retiree on a fixed dollar income, the remote worker who wants a base, or the investor chasing rental yield. For broader South America context, pair this with our cost of living in Argentina post and the moving to Uruguay guide.

The Per-Square-Meter Headline: Buenos Aires Is Genuinely Cheap

As of early 2026, here are the numbers I can defend with real listings:

- Buenos Aires (Palermo, Recoleta, Belgrano): USD $2,200-$2,800 per sqm for mid-tier apartments. Premium towers in Puerto Madero push $3,500-$4,500.

- Montevideo (Pocitos, Punta Carretas, Carrasco): USD $2,800-$3,400 per sqm for mid-tier. Oceanfront in Pocitos Nuevo climbs to $4,000-$4,500.

- Santiago (Providencia, Las Condes, Ñuñoa): USD $3,200-$4,200 per sqm for mid-tier. Vitacura and premium Las Condes hit $4,500-$5,500.

On a like-for-like 75 sqm two-bedroom in a well-regarded neighborhood, that works out to roughly $170K-$210K in Buenos Aires, $220K-$260K in Montevideo, and $250K-$320K in Santiago. Buenos Aires is 25-35 percent cheaper per sqm than Montevideo and 35-50 percent cheaper than Santiago. This is the biggest single fact in the comparison and it has been true in dollar terms since Argentina's 2018 currency crisis. The Benoit Properties Argentina 2026 market outlook and TheLatinvestor Argentina housing prices page both triangulate to the same range.

The catch: Buenos Aires prices are quoted in US dollars (and have been for 40 years, because nobody trusts the peso), but the Argentine macro picture is volatile enough that you need to understand what you're actually buying. More on that below.

Foreign Ownership Rules in All Three Countries

All three capitals allow foreigners to hold fee-simple freehold title in their own name, without residency, without a local company, and without a trust structure. This is the single biggest reason the Southern Cone is the easy part of Latin America for American buyers — no fideicomiso (Mexico), no restricted zones (Thailand/Philippines), no citizenship-linked ownership rules.

Argentina: Foreigners can own urban real estate outright. Rural land near borders and over certain hectare thresholds is restricted under Law 26.737 (the "Land Law"), but this does not affect apartment buyers. You need a CDI (Clave de Identificación) from AFIP, the tax authority, which functions as a tax ID for the transaction. The AFIP CDI application page explains the process. Escribano (notary) handles most of it.

Uruguay: The friendliest regime in South America. No restrictions on foreigners, no minimum investment, no residency requirement, no tax ID needed beyond a basic identification number issued at closing. The Uruguay Sotheby's foreign ownership FAQ and the GuruGuay property guide both confirm: passport + proof of funds + escribano and you are done.

Chile: Foreigners can own freehold in all urban areas. You must obtain a RUT (Rol Único Tributario, Chile's tax ID) from the Servicio de Impuestos Internos, which requires an in-person appointment or a power of attorney to a Chilean lawyer. Border-zone land (within 10 km of Argentina/Peru/Bolivia) has restrictions, which again do not affect Santiago apartments. The SII RUT application page and Global Property Guide Chile walk through it.

Firsthand buyer accounts: this r/expats thread on Buenos Aires purchases, the long-running BAExpats apartment buying forum, and r/uruguay threads on foreigner purchases are the three places to see what actually happens at closing.

What $200K Actually Buys in Buenos Aires

Buenos Aires at USD $200,000 is a genuinely good apartment in a genuinely good neighborhood. Here's the breakdown by barrio:

Palermo (the fashionable zone, split into Palermo Soho, Hollywood, Chico): A 70-85 sqm two-bedroom in a newer or well-maintained building, typically with balcony, 24/7 doorman (portero), and sometimes a pool/gym. Palermo Chico and Palermo Botánico are the premium sub-zones and push toward $250K for equivalent size. ZonaProp Palermo listings show current inventory.

Recoleta (old money, tree-lined, the French-architecture zone): Similar price per sqm to Palermo, but you typically trade some sqm for the address prestige. 65-75 sqm two-bedrooms at $180K-$220K in pre-war buildings (edificios antiguos) with high ceilings.

Belgrano (quieter, residential, excellent transit): 80-100 sqm two/three-bedrooms for $170K-$210K. Belgrano R (the most residential sub-zone) is where professional families cluster.

Puerto Madero (the luxury waterfront, newest buildings): $200K typically gets you a small 45-55 sqm one-bedroom. Good amenities, bad value per sqm. Americans who buy here are paying for the glass-tower skyline view and the security.

Villa Crespo, Colegiales, Caballito (the solid middle-class zones): 90-110 sqm two-bedrooms for $140K-$180K. Where locals with decent jobs actually live. Excellent value, less of a foreigner bubble.

Avoid: Puerto Madero if you're buying to live rather than to park dollars, anywhere advertised as "pozo" (off-plan — Argentine off-plan is a gamble given inflation), and ground-floor apartments in any barrio (security concerns in a city with periodic economic unrest). The Adventures in CRE Argentina deep dive has good discussion of the investor angle. Reddit threads on r/argentina for foreigners give the local-language view.

What $200K Buys in Montevideo

Montevideo is 20-30 percent more expensive than Buenos Aires per sqm, but it buys you into a far more stable legal and monetary system. Uruguay has not had a currency crisis in 24 years and its sovereign debt trades at investment grade, which matters when you are holding a dollar asset in a Latin American country.

Pocitos (the beachfront apartment neighborhood, the closest thing Montevideo has to Palermo): 60-75 sqm two-bedrooms in newer or renovated buildings for $180K-$240K. Oceanfront (frente al mar) adds 15-25 percent. Pocitos Nuevo has the tallest towers and the youngest demographic. The Mercado Libre Pocitos listings and InfoCasas Montevideo both show how thin the true mid-tier inventory is — newer buildings get bid up fast.

Punta Carretas (old-money, quiet, near the lighthouse and the shopping mall): 70-90 sqm two-bedrooms at $200K-$260K. The streets are leafy, the crime rate is low, and the address carries weight locally. Most foreign buyers end up here or in Pocitos.

Carrasco (the "Buenos Aires Belgrano" equivalent, eastern Montevideo, close to the airport): Houses and larger apartments. $200K buys a small 2-bedroom apartment in a newer building or stretches to a 3-bedroom in an older one. Carrasco is car-dependent.

Cordón, Centro, Tres Cruces: The more urban/central zones. $200K buys well — 80-100 sqm apartments in decent buildings — but the lifestyle is more city-downtown than beach-neighborhood.

Punta del Este (not Montevideo but worth mentioning): Two hours east, seasonal beach resort. $200K buys a small apartment in a tower away from Brava or Mansa beaches. Prices per sqm are closer to Santiago than Montevideo proper, especially in January-February season.

The La Cite Realtors buying guide and GuruGuay property costs article are the two best English-language walkthroughs. Reddit chatter is thinner for Uruguay than for Argentina, but r/IWantOut Uruguay threads and r/expats Uruguay have real-buyer anecdotes.

What $200K Buys in Santiago

Santiago is the most expensive of the three and the most "normal" — the closing process, the bank financing, the property records all function like a developed economy. You are paying the premium for that.

Providencia (central, professional, excellent transit on Line 1 metro): 55-70 sqm two-bedrooms in newer buildings at $200K-$270K. The classic Santiago neighborhood for foreign professionals. PortalInmobiliario Providencia listings and Toctoc.com are the two dominant portals.

Las Condes (the financial district, high-rise towers, American corporate expat zone): $200K gets you a modest 50-60 sqm one or small two-bedroom in a newer building, usually in the lower-tier blocks of Las Condes (closer to the Mapocho). Premium Las Condes (Cousiño, Nueva Costanera, Rosario Norte) is well above $200K.

Ñuñoa (the intellectual/bohemian middle class, excellent food scene, less towers): $200K buys a 75-90 sqm two/three-bedroom in a decent building. Better value than Las Condes on pure sqm, but less international and less amenity.

Vitacura (luxury, residential, houses and low-rise): Way out of budget at $200K. Median price well above $400K. Mentioned only to explain why it's on every "best neighborhood in Santiago" list and why you can't afford it.

Ñuñoa, La Reina, Macul: Middle-class zones with good green space and less foreigner premium. $180K-$220K gets you a quality 80-100 sqm apartment. Reddit discussions on r/chile buying property and r/santiago real estate have the local perspective.

Santiago's key distinctive: the local UF (Unidad de Fomento) pricing convention. Property prices are quoted in UF, not pesos, and the UF tracks inflation. Your Chilean mortgage is also denominated in UF. This is a good thing — it protects both buyer and seller from peso inflation — but you need to understand that a UF 5,500 apartment might cost 360 million pesos this week and 375 million pesos next month, even if the "price" hasn't changed.

Closing Costs Head-to-Head

Total closing costs on a $200,000 apartment, all-in, for an American buyer:

Buenos Aires, Argentina:

- Escribano (notary) fee: ~1.5-2% of sale price ($3,000-$4,000)

- Transfer tax (ITI, Impuesto a la Transferencia de Inmuebles): 1.5% on the seller, typically passed back to buyer via price negotiation

- Stamp tax (Impuesto de Sellos, CABA): 1.75% split 50/50, so 0.875% each ($1,750)

- AFIP registration and CDI: ~$100

- Real estate agent commission: 3% + VAT ($7,250)

- Lawyer (separate from escribano, highly recommended for foreign buyers): $1,500-$3,000

- Total buyer out-of-pocket: approximately $13,000-$16,000, or 6.5-8% of sale price

Montevideo, Uruguay:

- Escribano fee: ~3% of sale price ($6,000) — higher than Argentina because the escribano does more of the work

- Real estate agent commission: 3% + IVA 22% on the commission ($7,320)

- ITP (Impuesto a las Trasmisiones Patrimoniales): 2% split 50/50 ($2,000 buyer side)

- Registry fees and stamps: ~$600-$1,000

- Lawyer (optional — escribanos are lawyers in Uruguay): $0-$1,500

- Total buyer out-of-pocket: approximately $16,000-$18,000, or 8-9% of sale price

Santiago, Chile:

- Notary and Conservador de Bienes Raíces (public registry): ~$1,500-$3,000

- Real estate agent commission: 2% + IVA (paid by buyer, sometimes split) ($4,760)

- Transfer tax: effectively zero for residential under UF 2,000 equivalent, low otherwise

- Lawyer: $1,500-$3,000 (highly recommended for foreigners obtaining the RUT)

- Stamp tax on the mortgage deed if financing: 0.8% (financed buyers only)

- Total buyer out-of-pocket (cash buyer): approximately $7,000-$11,000, or 3.5-5.5% of sale price

Santiago is the cheapest to close, Montevideo is the most expensive, Buenos Aires is in the middle. Note that Uruguay's high closing cost is offset by the legal stability you get — the escribano-centric system is why title disputes are vanishingly rare. The GuruGuay closing cost breakdown and Adventures in CRE Argentina cover this in more depth.

How You Pay: Cash, Dollars, and the Argentine Twist

All three markets transact in or around US dollars, but the mechanics differ dramatically.

Argentina — physical cash is still normal: For decades, Buenos Aires real estate closed with literal briefcases of US dollar bills, counted and verified by the escribano on the closing day. Argentine banks are not trusted by Argentines and capital controls have made wire transfers painful. Recent reforms under the Milei government in 2024-2025 started allowing more normal electronic dollar payments, but cash-at-closing is still the default and you should plan for it. You'll open a local account at a dollar-friendly bank (Banco Galicia, Santander Argentina), wire from your US bank, withdraw the cash the morning of closing, and hand it over at the escribano's office. The BAExpats "Apartment purchase cost" thread has specific closing-day play-by-plays from actual American buyers.

Uruguay — clean wire transfers: Uruguay's banking system is the oldest and most trusted in South America. You wire USD from your US bank to the seller's Uruguayan bank account (or to the escribano's trust account), the escribano confirms receipt, and closing proceeds normally. Uruguayan banks (BROU, Itaú Uruguay, Santander) handle USD deposits without the Argentine drama. Plan 5-10 business days for the wire to clear. Wise/Western Union also work for smaller portions.

Chile — pesos at closing, USD at the start: Chile transacts in pesos, but listings are in UF and most foreign buyers bring USD. You wire USD to your Chilean bank (or to a currency exchange), convert to CLP, and show up at the notary with the certified cashier's check (vale vista) in pesos. Chile is the smoothest of the three for an American used to US closing mechanics.

FBAR/FinCEN 114 reminder for all three: Any non-US bank account holding more than $10,000 at any point during the calendar year triggers a US FBAR filing obligation. Americans buying in any of these three countries will almost certainly open a local account to pay taxes, utilities, and maintenance — file the FBAR. The IRS FBAR page and our avoid double taxation guide cover this.

Annual Carrying Costs and Property Taxes

This is where Santiago starts to look expensive and Buenos Aires starts to look like a bargain again.

Buenos Aires annual carry on a $200K apartment:

- ABL (municipal property tax, akin to US property tax): $400-$900/year — tiny by US standards

- Expensas (HOA equivalent for the building, highly variable): $1,200-$3,600/year for a typical mid-tier building; luxury buildings with 24/7 doorman/pool/gym push $4,800-$7,200/year

- Home insurance: $200-$400/year

- Utilities (electricity, gas, internet, water): $900-$1,800/year

- Total annual carry: approximately $2,700-$6,700/year

Note on expensas: this is the sleeper cost of Argentine apartment ownership. Inflation runs 80-150 percent annually in peso terms, and expensas rise with it. In dollar terms the rise is modest (because the peso depreciates), but if you are holding peso expenses against a USD-denominated asset, the variance can be unnerving. The expensas discussions on BAExpats have good numbers from current owners.

Montevideo annual carry on a $200K apartment:

- Contribución Inmobiliaria (municipal tax): $600-$1,500/year

- Impuesto al Patrimonio (wealth tax on urban property over UYU 5.3 million, applies selectively): $0-$800/year

- Gastos Comunes (HOA): $1,500-$3,600/year — Uruguayan buildings are well-maintained, fees reflect that

- Home insurance: $250-$450/year

- Utilities: $1,200-$2,400/year (higher than Argentina — Uruguay has expensive electricity)

- Total annual carry: approximately $3,550-$8,750/year

Santiago annual carry on a $200K apartment:

- Contribuciones (Chilean property tax): $0-$1,800/year — below UF 883 fiscal value apartments are exempt; most $200K Santiago apartments sit above this and pay ~1% annually on the fiscal value (usually 50-70% of market)

- Gastos Comunes: $1,800-$4,200/year — Santiago high-rises have doormen, gyms, pools, and they aren't cheap

- Home insurance: $300-$500/year

- Utilities: $1,200-$2,400/year

- Total annual carry: approximately $3,300-$8,900/year

On pure carry cost, Buenos Aires wins. On predictability and dollar stability, Santiago wins. Montevideo sits in the middle on both.

Visa Paths and Why They Matter

Owning property in any of these three countries does not automatically give you residency — but each country has an accessible pathway that pairs well with a property purchase.

Argentina — Rentista visa: Demonstrate USD $2,000-$2,500/month of passive income from outside Argentina (pensions, rental income, dividend income, Social Security). One-year renewable, converts to permanent residency after three years, citizenship eligible after two years of legal residency. The Argentine Ministry of the Interior migrations page has the official list. Argentina is famously relaxed about overstays (three-month tourist visa, easy to extend/renew), so many American expats just live there informally for years before getting serious about residency. The r/AmerExit Argentina threads have real visa experiences.

Uruguay — Residencia Legal / Rentista: Demonstrate $1,500-$2,500/month passive income, or make a "significant investment" (typically interpreted as buying property worth $525,000+ or business investment). The property-investment path is direct: buy an apartment, apply for residency, done. Processing takes 6-18 months. Permanent residency after 3-5 years, citizenship at 5 years (or 3 with Uruguayan spouse). The Ministerio del Interior Uruguay residency page has details. Uruguay is famous for the "digital nomad" tax residency rules (you become a tax resident but pay no tax on foreign income for the first 10 years — the "tax holiday").

Chile — Temporary Resident Visa / Rentista: Demonstrate passive income of at least ~USD $1,500-$2,500/month. Valid for 1-2 years, renewable, converts to permanent after 1-2 renewals. The Departamento de Extranjería y Migración Chile manages the process. Chile recently tightened migration rules (2022-2024) in response to Venezuelan migration and the process is slower than it used to be, but still accessible for American retirees with documented income.

For all three, owning a home helps at application time — it demonstrates ties and "intent to reside" — but is not a legal substitute for the income test. Our cheapest countries for residency and property post compares these visa thresholds against the rest of the world.

Tax on Rental Income and Capital Gains

Before you buy, understand what happens when you rent the place out or sell it.

Argentina: Rental income is taxed at progressive rates on non-residents (15-35%) with no basic exemption for non-residents in theory, though in practice Argentines (including non-resident owners) informally under-declare. Don't do this as an American — the IRS requires worldwide income reporting and the gap between what you report to AFIP and what you report to the IRS will flag on audit. Capital gains: 15% for non-residents on the real (inflation-adjusted) gain. Argentine law allows cost-base indexing, which is generous. AFIP property tax FAQ has the current schedules. The r/tax Argentina threads have American-specific angles.

Uruguay: Non-resident rental income is taxed at 12% flat (IRNR — Impuesto a la Renta de No Residentes), no exemptions. Capital gains: 12% on the nominal gain, which is a bit painful because there's no indexation (you pay on inflation too). Uruguay's general tax regime is famously clean — the DGI Uruguay page and the Guru'Guay tax overview walk through it. Uruguay has no worldwide tax on new residents for 10 years, which is unique in the region and very valuable for Americans with significant passive income.

Chile: Non-resident rental income is taxed at a 35% withholding rate, though actual effective rate after deductions usually lands at 20-25%. Capital gains: 10% flat for individuals on residential property, with a lifetime UF 8,000 exemption (approximately $330K) for primary residences. The SII Chile foreigner guide explains. Chile has a US double-taxation treaty (Argentina and Uruguay do not), which is a meaningful benefit for Americans — you can credit Chilean taxes paid against US tax liability more cleanly.

Practical takeaway: if you plan to rent out, Chile's DTA is the single biggest tax advantage. If you plan to live in the property as a new tax resident, Uruguay's 10-year tax holiday is the single biggest tax advantage. Argentina has neither, but the purchase price is so much lower that the math still often works for live-in buyers.

Macro Risk: What Could Go Wrong in Each

These are all Latin American economies with histories of volatility. Here's the honest risk picture:

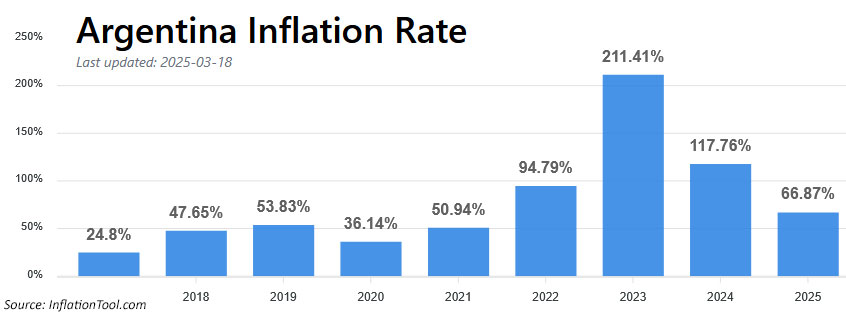

Argentina: The single biggest risk in the region. Argentina has defaulted on sovereign debt nine times since 1816 and suffered currency crises in 2001, 2014, 2018, 2019, and 2023. Inflation hit 200%+ annualized in 2023-2024 before the Milei administration's shock-therapy reforms started to bring it down. Why buying can still make sense: real estate in Argentina is priced in dollars, not pesos, and the dollar price generally holds (or rises) during peso crises because local Argentines rush into real estate as an inflation hedge. You are essentially buying a US-dollar asset in a country with periodic instability. The currency crashes hurt your daily living costs (if your income is in dollars) less than they hurt your asset value (which is already dollar-denominated). The Adventures in CRE Argentina analysis makes this case in detail.

Uruguay: The lowest macro risk on the continent. Uruguay has had investment-grade sovereign debt since 2012, no currency crisis since 2002, stable democratic institutions since 1985, and a functioning independent central bank. The downside is there are only 3.4 million Uruguayans, the economy is tiny, and if you need to sell your apartment quickly the buyer pool is limited — your exit liquidity is thinner than in Argentina (larger market) or Santiago (wealthier buyers).

Chile: Moderate risk. Chile had a famously stable economy for 30 years (1990-2019), then the October 2019 "estallido social" protests sparked a period of political uncertainty, a new (rejected) constitution in 2022, a second (rejected) constitutional proposal in 2023, and the Boric government's policy shifts. The peso has weakened and property prices in USD terms have dropped 10-15% from 2019 peaks in premium areas. The institutional framework (rule of law, property rights, banking) is still the strongest of the three. The Global Property Guide Chile market commentary tracks this well.

Scam/fraud landscape: Argentina has the highest incidence of title issues and "escribano doesn't pay" problems — because cash-heavy closings create opportunities. Uruguay has almost none. Chile has modern digital registries and low fraud. If you're paranoid about title problems, that's another point for Uruguay/Chile. Our common scams post has the broader Latin America scam landscape, which applies partially here.

Who Should Buy Where

The honest matching:

Buy in Buenos Aires if: You want the biggest apartment for your dollar, you enjoy a dense European-style urban culture (cafés, theaters, bookstores, nightlife), you can tolerate macro volatility in exchange for asset-level dollar stability, and you value the Rentista visa's eventual citizenship pathway at two years. Buenos Aires is the single best South American capital for Americans who want maximum quality-of-life-per-dollar and don't need institutional comfort.

Buy in Montevideo if: Legal certainty matters more than sqm-per-dollar, you want the 10-year tax holiday on foreign income, you plan to use Uruguay as a base for both residency and tax migration, and you value quiet over chaos. Montevideo is the right call for Americans moving serious wealth out of the US — the tax holiday alone justifies it for anyone with $200K+/year of portfolio income.

Buy in Santiago if: You want the most institutional experience closest to US norms, you need Chilean banking and mortgage financing (Santiago is the only one of the three where a foreigner can reliably get a local mortgage), and you're willing to pay a 30-50% premium for stability and infrastructure. Santiago is the best call for American professionals on corporate assignments, families with school-age kids, and anyone who wants minimal drama.

Skip all three if: You can't tolerate 11-hour flights from the US, you're buying purely as a rental-yield investment and don't care about lifestyle, or you don't speak any Spanish and aren't willing to learn functional conversational Spanish — none of the three are Anglophone and the bureaucracy is all in Spanish.

For live inventory in all three cities, see our Argentina country page, Uruguay country page, and Chile country page. For broader comparisons, our cheapest cities abroad post and cost of living in Argentina are the next reads. If you want to compare against other cheap Latin American capitals, our Medellín vs Cuenca vs Panama post is the closest companion piece.

The meta-point: Southern Cone real estate is the easy part of Latin America for an American buyer. No fideicomiso, no restricted zones, no spouse-workaround schemes. You walk into an escribano's office, wire dollars, sign, and own freehold in your own name. That alone justifies a closer look — and the per-sqm prices, especially in Buenos Aires, are the cheapest in any G20-adjacent economy right now.

Ready to explore?

Browse Destinations